Creating a personal budget is one of the most effective ways to gain control over your finances. Whether you’re earning a fixed salary, juggling multiple freelance gigs, or dealing with an unpredictable income, budgeting helps you allocate your money efficiently, plan for the future, and avoid unnecessary stress.

In this guide by Cash and Coffee Club, you’ll learn how to make a budget based on income, no matter your financial situation. We’ll also explore popular budgeting methods like the 50/20/30 rule, 70/20/10 method, and zero-based budgeting, with tips for high earners and those with fluctuating income.

Why Budgeting Matters?

Budgeting isn’t just about numbers—it’s about taking control of your financial future. Without a clear plan, money can easily slip through your fingers, leaving you wondering where it all went at the end of the month. A well-structured budget helps you align your income with your goals, ensuring that every dollar has a purpose.

When you create a budget, you’re doing more than just tracking expenses. You’re making intentional financial decisions that support your lifestyle, values, and long-term aspirations. Whether you’re saving for a dream vacation, paying off debt, or building an emergency fund, budgeting provides the structure and clarity you need to succeed.

>> See more: Best Budgeting Apps in 2025

It also reduces stress. Financial uncertainty is one of the leading causes of anxiety, but having a plan in place gives you confidence and peace of mind. You know how much you can spend, what you need to save, and how to prepare for the unexpected.

Most importantly, budgeting empowers you. It puts you in the driver’s seat of your financial life. You stop reacting to money problems and start proactively managing your wealth, no matter how much you earn. Whether you make $2,000 or $20,000 a month, budgeting is the key to building financial stability, reaching your goals, and living with greater freedom and security.

Step-by-Step: How to Make a Budget Based on Income

1. Calculate Your Total Monthly Income

The first and most essential step in creating a budget is knowing exactly how much money you bring in each month. This total income serves as the foundation for all your financial planning. Without a clear understanding of your income, any budget you create will be incomplete or inaccurate.

Start by identifying all sources of income—not just your regular paycheck. This includes:

Salary or wages (after tax deductions)

Freelance or gig work (Upwork, Fiverr, Uber, etc.)

Side hustles (online business, tutoring, content creation)

Rental income (if you own property)

Investment income (dividends, interest, etc.)

Child support, alimony, or government benefits (if applicable)

Bonuses and commissions

If your income is fixed, this step is simple. But if your income varies each month—as is common for freelancers or gig workers—it’s important to calculate your average monthly income. A good strategy is to take your earnings from the last 3 to 6 months and find the average. Alternatively, you can base your budget on your lowest-earning month to be more conservative.

💡 Pro Tip: Wondering how to budget with no set income? Always plan for the worst-case scenario—use your minimum income as your budget base and adjust when you earn more.

Knowing your total income gives you the clarity to make informed decisions about how much you can spend, save, or invest. Once this number is clear, you’re ready to move on to tracking expenses and building a spending plan that truly fits your lifestyle.

2. Track and Categorize Your Expenses

Break your spending into fixed and variable categories:

Fixed Expenses: Rent/mortgage, insurance, loan payments

Variable Expenses: Food, utilities, entertainment, transportation

Discretionary Spending: Subscriptions, shopping, dining out

Use budgeting apps like Mint, YNAB (You Need A Budget), or a simple spreadsheet to log your expenses.

3. Choose a Budgeting Method That Works for You

There’s no one-size-fits-all solution. Explore these popular strategies:

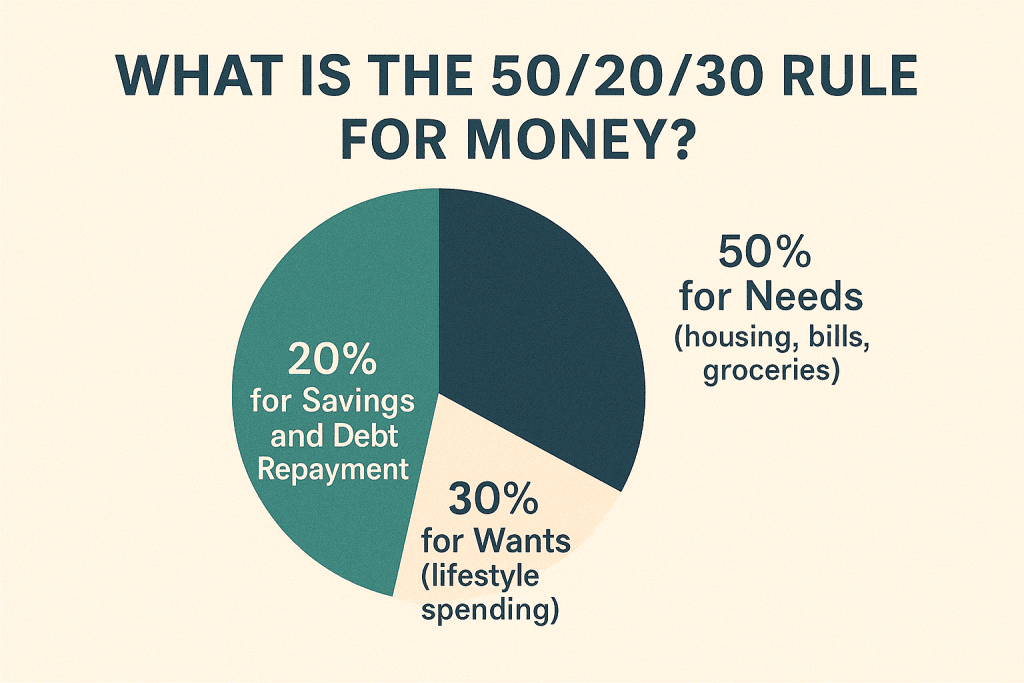

🔹 What is the 50/20/30 Rule for Money?

This method divides your income into three buckets:

50% for Needs (housing, bills, groceries)

20% for Savings and Debt Repayment

30% for Wants (lifestyle spending)

It’s a great starting point for beginners who want balance and flexibility.

🔹 What is the 70/20/10 Rule for Money?

A more aggressive savings approach:

70% for Living Expenses

20% for Savings

10% for Debt or Giving

Perfect if you’re focused on reducing debt or building long-term wealth.

🔹 What is the 50/25/25 Rule?

A slight variation offering more focus on saving:

50% for Essentials

25% for Savings & Investments

25% for Personal Spending

This method is ideal for those with higher income who want to build wealth faster.

🔹 What is the Zero Budget Method?

Every dollar you earn is assigned a purpose until your income minus expenses equals zero.

This detailed method forces intentionality and is perfect for anyone asking, “How do I create a realistic budget?”

Bonus: Use this method if you need structure or tend to overspend.

Adjusting for Different Income Levels

✅ Budgeting for Low or Irregular Income

Use a bare-bones budget: Focus only on essentials

Prioritize emergency savings

Automate what you can during higher-income months

Track income fluctuations closely

This answers: “How to budget with no set income?”

How Do You Budget for High Income?

Having more income doesn’t mean you’re exempt from budgeting. In fact, it’s more important than ever.

Avoid lifestyle inflation

Maximize retirement contributions (401(k), IRA)

Use the 50/25/25 or zero-based method

Track spending to stay grounded

Tips for Creating a Realistic Budget

Here’s how to make your budget sustainable and realistic:

Set achievable goals: Start small if needed

Leave room for fun: Deprivation causes burnout

Review monthly: Adjust as life changes

Use tools: Budgeting apps can automate the process

Involve your partner or family if applicable

Asking “How do I create a realistic budget?” Start by keeping it simple and flexible.

Sample Monthly Budget Based on Income

| Income | $4,000/month |

|---|---|

| 50% Needs | $2,000 |

| 20% Savings/Debt | $800 |

| 30% Wants | $1,200 |

This follows the 50/20/30 rule, which can be adjusted as your priorities shift.

Common Budgeting Mistakes to Avoid

Ignoring small expenses

Not tracking cash flow

Failing to adjust your budget regularly

Overcomplicating your plan

Forgetting irregular expenses (gifts, insurance premiums)

Final Thoughts: Find the Budget That Works for You

Budgeting isn’t about restriction — it’s about empowerment. Whether you prefer a zero-based budget, the 50/20/30 rule, or need a method for fluctuating income, the key is to stay consistent and adjust when needed.

No matter your income level, budgeting gives you control, clarity, and confidence with your money. So don’t wait — take the first step today.